Property Tax Increases for Arizona Homeowners

September 22, 2015

Charles “Hos” Hoskins

Maricopa County Treasurer

In 2012, voters passed Proposition 117 hoping to see a property tax reduction; however, it probably won’t work out that way for most homeowners. Before I tell you why, let me cover some of the characteristics of the Arizona property tax system.

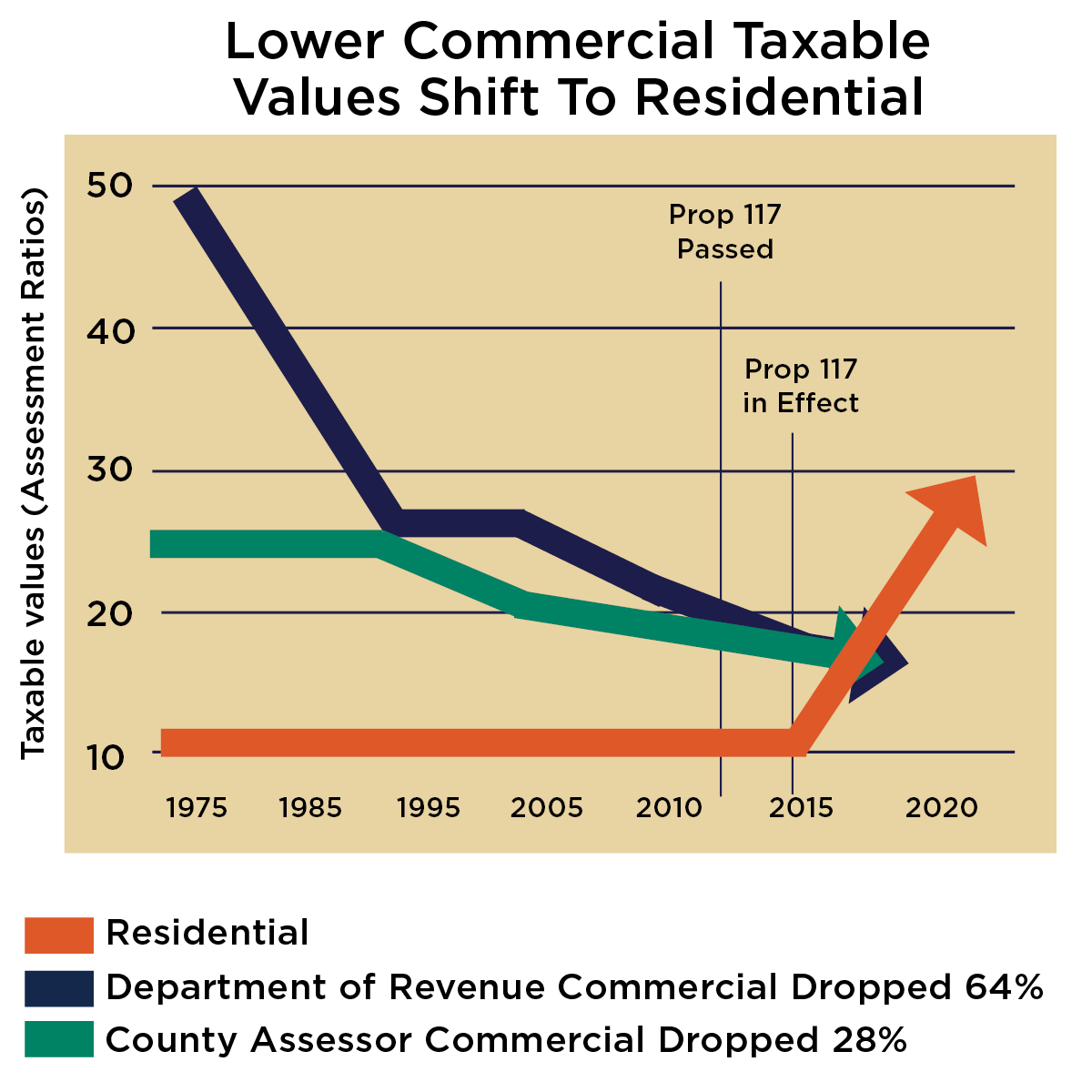

Properties are classified by use with two major classes: commercial and residential. Commercial properties consist of all income producing properties from electric generating plants to a small mom and pop restaurant. The larger commercial properties such as mines, utilities, railroads, airlines, pipelines, telecommunication and others are valued by the Arizona Department of Revenue (DOR). Income producing properties such as shopping centers, manufacturing, general businesses and others are valued by the county assessor. Residential properties defined as rentals, owner occupied primary and non-primary homes are also valued by the county assessor.

The DOR and county assessor place two values on each property referred to as full cash and limited values. Beginning this year, both primary and secondary taxes will be levied against the limited value. Primary taxes are used to fund the operating budgets of the county, cities, schools and community colleges. Secondary taxes fund approximately 1,400 special district budgets (hospital, fire, library, water, street lights and others) and approximately 350 voter approved bonds and budget overrides. An average of 10 to 15 separate districts tax each property.

The limited value is factored by an assessment ratio set by the legislature to determine the assessed value which is the taxable value. The assessment ratio for residential properties has been 10 percent since 1973. The ratio for most DOR valued commercial properties was 50 percent in 1979, gradually dropped to 25 percent by 1999, dropped to 20 percent in 2012, and will drop to 18 percent in 2016 for a total drop of 64 percent. Commercial properties valued by the county assessor had an assessment ratio of 25 percent through 2005; it dropped to 20 percent in 2012 and will drop to 18 percent in 2016 for a total drop of 28 percent. All of these reductions in taxable value were enacted by the legislature at the urging of lobbyists hired by owners of large commercial properties.

When the legislature reduces the taxable value of one class of property by lowering the assessment ratio it shifts the tax burden to other classes, mostly residential. Reducing the limited value of DOR valued commercial properties by 64 percent and county assessor valued commercial properties by 28 percent has increased homeowner’s annual taxes by 20 to 30 percent. If a homeowner divides their tax by five it will give a rough estimate of how much more taxes were owed just in 2015 due to these taxable value reductions.

The amount of tax is determined by the tax rates set by each tax district. The tax rate is calculated by dividing the tax district’s budget by the total limited assessed value in the district. That rate is applied to the assessed (taxable) value of each property to determine what share of each district’s budget it will pay. Reducing assessment ratios for commercial properties reduces the total limited assessed value that is divided into the district’s budget causing a higher tax rate – shifting the burden to those properties whose taxable values remained the same, mostly residential.

This burden shift to residential properties caused by both market changes and special interest legislation will be locked in for many years due to passage of Proposition 117 in 2012. Prop 117 will neither lower nor raise total property taxes. It will, however, lock in the tax burden shifts caused by the greater market increases of residential properties that occurred during the three years from when it passed in 2012 and when it became effective this year in 2015.

Prop 117 requires all taxes to be levied against the assessed limited value and limits yearly increases of the limited value to five percent – not to exceed full cash value. In 2012, the gap between full cash and limited values for both residential and commercial properties was less than one percent. In 2015, the gap for DOR valued properties is still less than one percent, but it’s 8.9 percent for commercial properties valued by the county assessor and about 19.2 for all residential properties.

There are numerous possibilities depending on what happens to market values of residential and commercial properties. However, if current full cash values were frozen, residential properties would experience the full five percent increase in taxable value for four years while commercial properties would receive the maximum increase for only two years. If the full cash value of residential properties increases at least five percent each year, the tax burden shift from recent market increases and ongoing tax breaks for commercial properties will never be overcome due to Prop 117. You can search (google) “property value limits” online and find numerous articles written by economist and university professors describing how valuation limits will shift the tax burden to residential properties.

Another factor is Prop 117 becoming effective during a year where the assessment ratio for all commercial properties dropped from 19.0 percent to 18.5 percent. This reduces the Prop 117 five percent increase in limited value for all commercial properties in 2015 to only 2.37 percent [5.0 – (0.5 ÷ 19.0) = 2.37]. In 2016, it will only increase 2.3 percent when the ratio drops to 18.0 percent. This means that the taxable value of commercial property can only increase about 4.7 percent for the first two years. Prop 117 is effective while taxable value of residential property can increase the full 10 percent.

All this will lead to ongoing higher taxes for residential properties that experienced higher increases in market value the last two years.