Mortgage Bankers Association Arizona Update

March 28, 2016

Joel Kan

Associate Vice President, Industry Surveys and Forecasting Mortgage Bankers Association

In the Mortgage Bankers Association (MBA) most recent Mortgage Finance Forecast, revisions to national mortgage origination estimates for 2015 through 2018 were made. The 2015 originations total was revised from $1.49 trillion to $1.63 trillion including upward revisions of purchase originations for 2015 from $821 billion to $881 billion. Refinance originations from $665 billion to $749 billion were also adjusted. Generally, the adjustments were the result of reexamining data on 2015 applications, pull-through rates and other factors impacting originations. Expectation for both purchase and refinance originations were also raised in 2016 given the higher starting point and also a lower rate outlook for 2016. Despite the recent surge in refinance activity as rates have dropped, we still expect to end the year in a purchase dominated market.

Furthermore, the MBA National Delinquency Survey for fourth quarter 2015 showed continued improvement in the performance of loans held by Arizona borrowers. The serious delinquency rate, which includes all loans in the foreclosure process and loans that are ninety days or more past due, dropped to 1.68 percent from 1.72 percent in the previous quarter and from 2.25 percent in the fourth quarter of 2014. The foreclosure starts rate remained unchanged from the third quarter of 2015 at 0.23 percent, still down from 0.32 percent the previous year. Arizona continues to perform significantly better than the United States average, whose fourth quarter 2015 serious delinquency rate was 3.44 percent and foreclosure starts rate was 0.36 percent.

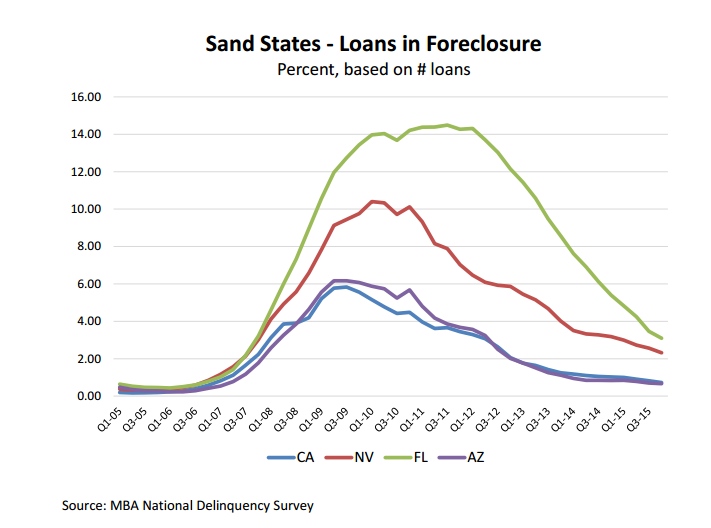

Arizona is one of the so-called “sand states” where markets continue to see drastic improvements in terms of their percent of loans in foreclosure, although Florida and Nevada have yet to return to pre-crisis levels. Following the recession, Florida not only had the largest percent of loans in foreclosure, but was also a judicial state and saw a huge backlog in the foreclosure pipeline. As housing markets recovered in Florida, the percent of loans in foreclosure started to decline more rapidly. Arizona and California, both non-judicial states, saw a much quicker recovery in comparison.

As the job market strengthens and as home prices continue to grow and stabilize, we expect recent loan origination vintages will continue to show strong performance with fewer serious delinquencies. Older vintages have benefited from these favorable market conditions as well, resulting in fewer new foreclosures, and more opportunities to be resolved for those who have fallen behind in their payments.

However, there were increases in the foreclosure starts rate in a handful of states that have economies closely tied to the oil industry. Out of 12 states that had an increase in foreclosure starts in fourth quarter 2015, five of those were in states with oil-dependent local economies. Oklahoma, North Dakota, Louisiana, Colorado, and Texas saw increases in new foreclosures while the national average continued to trend lower. Employment trends in each of these states were running below the national average during 2015, as employment in oil and gas related industries continued to decline.

Recent data also shows that four of the five states (with the exception of Colorado) were ranked among the 10 weakest states in terms of second quarter 2015 real GDP growth. Oklahoma’s economy in particular contracted by 2.4 percent in the second quarter (the latest quarter for which state data is available). It also suffered the largest increase in foreclosures starts during the fourth quarter according to the NDS, increasing by 13 basis points.