Arizona Multifamily Market Trends and Investments

July 7, 2017

By John Kobierowski and Thomas Brophy, ABI Multifamily

Despite stocks hitting all-time highs, markets across the globe have been prone to ever increasing volatility fits. As a result, middle age-to-older market investors have been switching to a combination of passive ETF funds and purchasing a mix of closed-fund shares and/or direct investments in real estate to provide more consistent returns. This change in investor sentiment, ceteris paribus, will continue to propel real estate transactions, particularly multifamily, into the foreseeable future.

Phoenix MSA and Tucson MSA witnessed substantial y-o-y increases in units delivered to the market at 37 percent and 90 percent in 1Q. Despite the substantial increase in deliveries, occupancy rates in the multifamily market which remained at historical highs of 94 percent+ for the region, fueled in a large part by sustained job and population growth. How does this compare to the rest of the region and nation?

The Prominent Investors in the Arizona Market California-based investment groups, fueled largely on investor money fleeing the negative interest rate doldrums of Asia and Europe, as well as California individual and family investors lead the pack in number of units purchased in Arizona. In fact, California investors purchased nearly 40 percent of all multifamily units sold in Arizona as a whole in 2016, up 4 percent from 2015 – with no signs of dissipation in 2017. In addition to California investors, New York, Utah, Pacific Northwest and Canadian investors significantly increased their holdings over the same time period.

While single-family home construction in Arizona is rebounding – but still far from normal. Home builders have been struggling with a number of issues from labor shortages, rising material costs and lack of available land, particularly in more urban core areas. Of particular note at a recent Infill Conference, there is a consensus among builders, developers and investors that the wave of Californians moving to Arizona has only begun – and mimics Silicon Valley’s morph into the Silicon Desert.

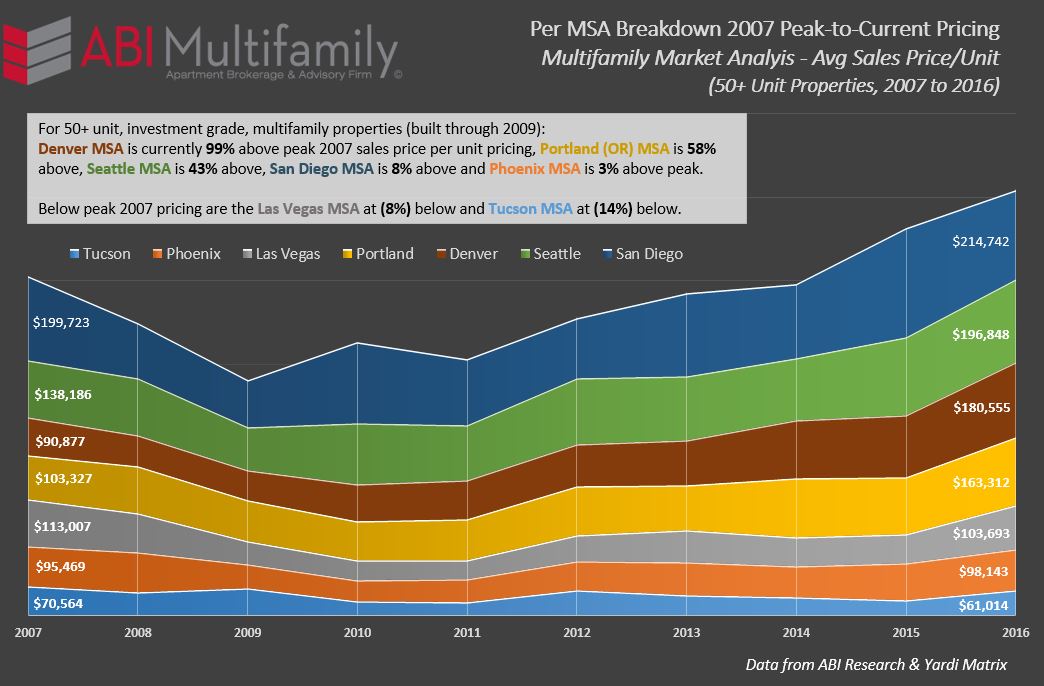

Price Comparisons and the Market On more than one occasion we have heard that 2005 marked the beginning of the end for the previous bull market. Arguments can be made that it started earlier for some places; however, on the whole this hypothesis holds merit. With this in mind, we ask the following question:

If 2005 was the last year of ‘sane’ investment/building prior to the 2007/08 Great Recession, what would the price per unit be now (YE 2016) if average price-perunit growth was a more modest 3 percent per annum, compounded?

The answer is very surprising. For Phoenix MSA, the average price-per-unit sold in 2005 was $67,199. Based on the question above, the projected price-per- unit would have been $95,810. Phoenix’s 2016 actual average price-per-unit was $98,143 or 2.5 percent greater than if the 3 percent growth had been maintained. On the other hand, Tucson would be at $74,194 which is substantially higher than its current $61,014.

As referenced in the chart, most of the Western MSA’s have broken their previous 2007 peak average price-per-unit record with the exception of the Las Vegas and Tucson MSA’s. It should be noted that while an MSA’s average price per unit amount can exceed its previous peak this does not apply to all year built/class types. For example, Phoenix MSA is currently 3 percent above its average 2007 peak, Pre-1980′s, 1990-99 and 2000-09 built product are on average (4 percent) below their previous peak.

The Western U.S., with an average growth rate of approximately 30 percent, is two times higher than that of the U.S. over the same sixteen year time period. In fact, Maricopa County (Phoenix MSA) recently overtook Harris County, Texas as the fastest growing county in the nation – averaging 222 new residents per day from 2015 to 2016.

The net result: interest in multi-family investments in the Southwestern U.S. will remain elevated as investors look for yield and people seek new places to live and work.

John Kobierowski is co-founder and Senior Managing Partner at ABI Multifamily with over 25 years’ experience in the multifamily industry. During his tenure, John has closed over 900+ multifamily transactions with clients ranging from national/institutional investors to regional syndicators and local operators.