Market Summary

July 7, 2017

Michael Orr

Founder and Owner, The Cromford Report

We see a housing market in Greater Phoenix that is continuing to strengthen almost across the board. Many of the trends that were visible in 2015 and 2016 have continued into 2017 with little change except they have become more apparent.

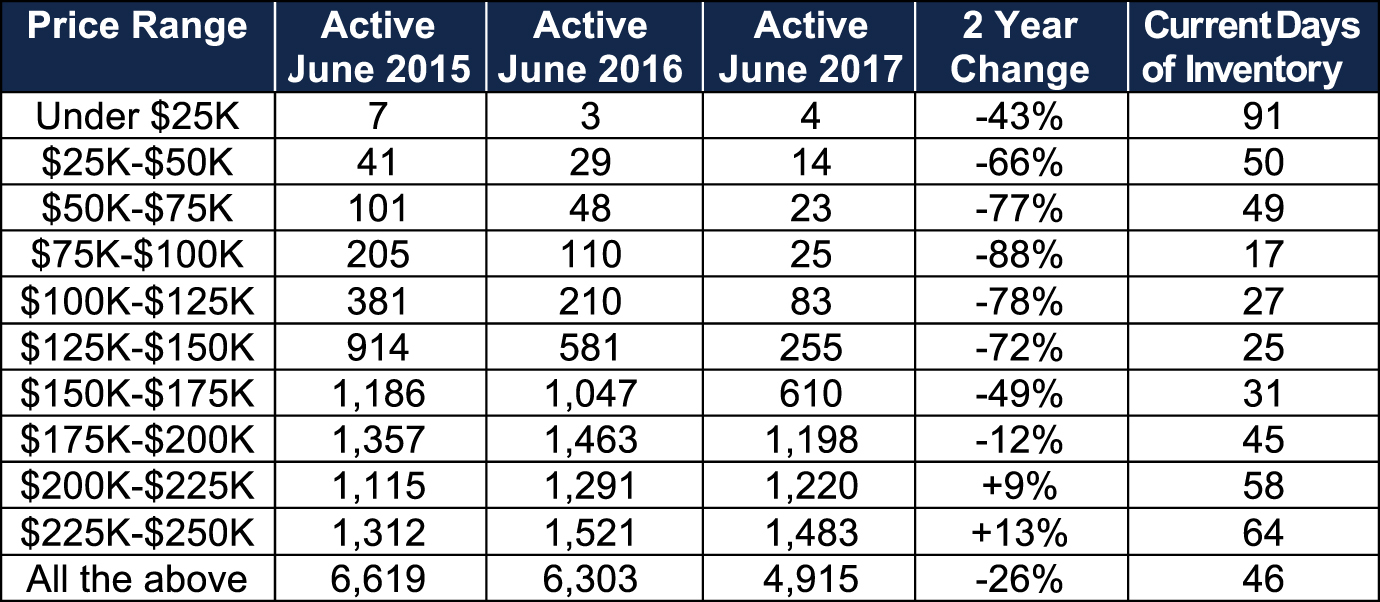

At the affordable end of the market, we have even fewer homes available. Looking at the active single-family listings listed as available for sale with or without an existing contract we see the following numbers by price range:

Below $175,000 there are just over 1,000 single-family homes offered for sale. It is worth remembering how this contrasts with June 2011 when there were over 14,000. Those that are offered tend to sell very quickly. Inventory (measured against the annual sales rate) for the segment under $175,000 is now down to 29 days. Since this number includes active homes that already have a contract (UCB and CCBS status), anyone trying to buy a single-family home under $175,000 is going to be faced with a very high level of competition from other buyers, which drives prices up and aggravates the supply problem yet further.

Once we reach $200,000 the situation eases and we actually have more active listings than in 2015. However, the annual sales rate for homes between $200,000 and $250,000 has shot up by 47 percent from 10,945 to 16,080 over the past 2 years. This means that the days of inventory measure has declined despite the higher active listing count.

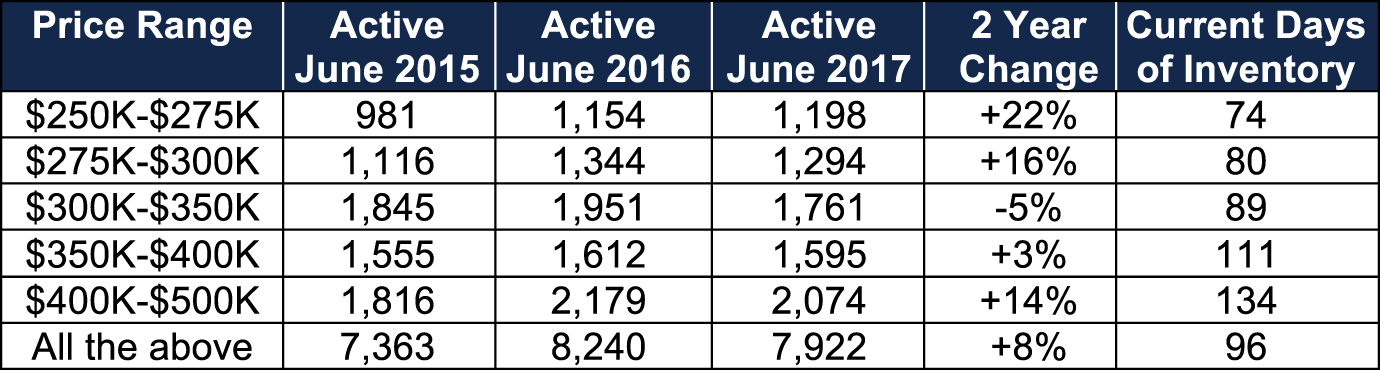

In the mid-range the situation looks like this:

The number of active listings is 8 percent higher than 2 years ago, so at first sight the market looks well-supplied. However, the annual sales rate has increased almost 50 percent from 20,012 to 29,982, so the extra supply is completely dwarfed by the growth in demand. Inventory has declined from 134 to 96 days which means sellers have the advantage and so continued appreciation is in the short-term forecast.

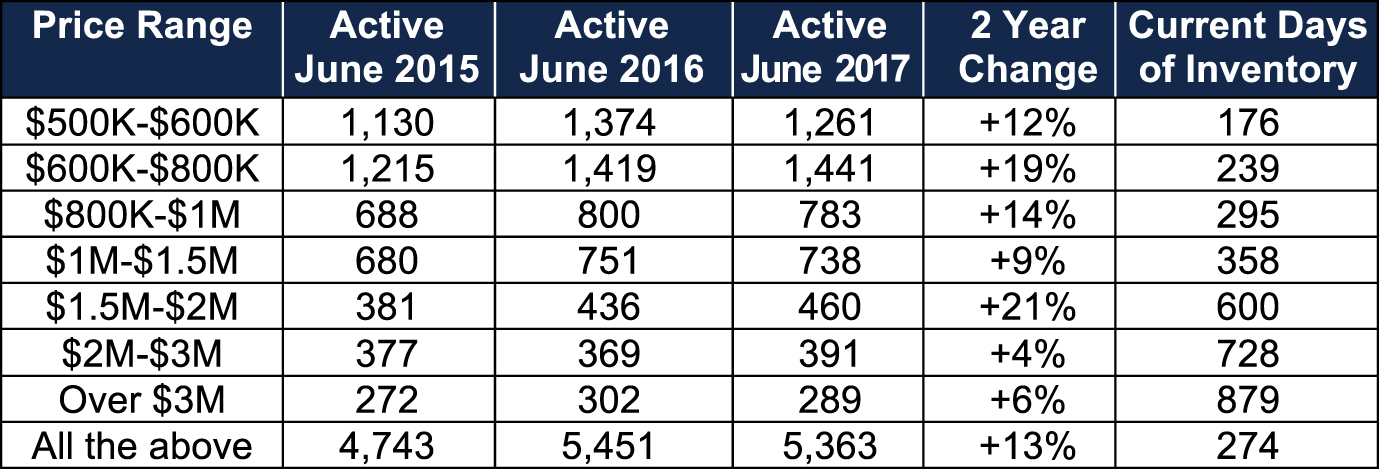

Above $500,000 the picture is rather different:

We have 13 percent more supply than 2 years ago, so there is still plenty of choice for buyers. However, the annual sales rate for homes over $500,000 has increased from 5,264 to 7,132, a rise of 35 percent. So here we can see that the growth in demand is faster than the growth in supply and after a weak period since peaking in mid-summer 2015, prices in most luxury areas are on the rise again, particularly for homes under $1.5 million. It is above $1.5 million where the market starts to change for the worse.

We can see that inventory is over 600 days from homes priced above $1.5 million, and here annual sales have risen from 547 to 596, an increase of only 9 percent, while supply is up by from 1,030 to 1,140, a rise of 11 percent. Now we see a problem. When supply increases as a faster rate than demand, sellers are at a disadvantage. Pricing will have a hard time making substantial upward progress until this condition changes.

Of course the market over $1.5 million is only a tiny segment compared to the market as a whole. It represents just 0.8 percent of units sold though a more significant 6.9 percent of dollars spent.

Below this price point we are seeing a few growing trends:

• New homes are growing market share over re-sales

• Attached homes (condos / townhomes / duplexes, etc) are growing market share over single-family homes

• Homes that are close to attractive facilities (especially if they are walkable) are gaining market share over homes in the distant fringes of the built-up areas

With underwriting standards relaxing, we see continued strength in demand ahead, coupled with ongoing shortages of supply at price points below $500,000.